2b/2 BABA: Back for Business

New management, new strategy, new growth opportunities

In the previous two parts (part 1 and part 2a) in this series, we outlined the numerous missteps that Alibaba took along its journey and why it struggled.

We now examine in detail the risks associated with Alibaba and what has changed to make us much more optimistic about the company – as recently as February this year, we were very bearish on the company.

As for most equities, investors are compensated for bearing three major types of risks when it comes to Alibaba (the types of risks remain the same while the risks themselves will differ):

Country risks. These include for example US-China geopolitics & pessimism around the Chinese economy.

Sector risks. Domestic Chinese politics and policies against Big Tech.

Idiosyncratic risks. Business fundamentals, especially of Alibaba’s core ecommerce business.

To be clear, these are not equally important; idiosyncratic risks, driven by business fundamentals, outweigh the other two in terms of importance.

The evidence? Check out the charts below: the first shows Alibaba’s quarterly year-on-year revenue growth, while the second shows the share price over the corresponding period. Look closely and it would even be possible to determine how specific peaks and troughs correspond.

The reason for this high correlation is simple: Alibaba has long been seen as a growth stock, and its stock price is, to a significant degree, determined by its perceived potential for growth.

“When investing, we view ourselves as business analysts — not as market analysts, not as macroeconomic analysts, and not even as security analysts.”

-Warren Buffett

We must guard against availability bias, which afflicts many investors, including even professionals.

Because Alibaba is listed in the US and Hong Kong, and because of the PRC’s restrictive capital controls, most of Alibaba’s core customers have only limited access to this market.

It should be noted that most Hong Kong investors, too, lack immediate awareness of major developments, with key digital players being conspicuously absent from the Hong Kong market.

For example, the Chinese version of TikTok, Douyin, is not available in Hong Kong. In fact, residents in Hong Kong would only rarely use Chinese social media or apps. Only a small – though growing – subset of Alibaba’s services is available to the city.

As a result, most investors who do have access to Alibaba have limited understanding of its core business. Very understandably, they accord the most weight to the factors that they have the highest visibility of, which are most reported in non-Chinese media.

Unfortunately, or fortunately for value investors with long time horizons, many market participants attribute Alibaba’s share price to global or domestic Chinese politics (the first two factors), due to availability bias – it is much easier for many investors to think of examples of macro rather than specifics.

Market inefficiency, arising from this information asymmetry, permits what we believe to be an asymmetric bet on Alibaba for investors in the know.

In short, then, we posit that for Alibaba, macro factors are largely subordinate in importance to business fundamentals, and should principally be assessed in how they would affect business.

Of course, in the short term, sentiment-related risks may have significant impact.

Country Risk

There are four major risks:

China hard landing risk

Tariffs and other geopolitical risk

Delisting risk

VIE risk

We go through each by turn. Country risk is a subject that warrants a series of its own, so we shall only touch upon those aspects that most directly pertain to Alibaba.

China hard landing risk. We are moderately optimistic about China’s economic prospects – and that of the US as well, where many of Alibaba’s investors are.

The Q1 GDP numbers came out recently, showing a 5.3% growth year-on-year and beating expectations, despite a 7.5% fall in exports.

“Online retail sales reached 3,308.2 billion yuan, up by 12.4 percent year on year. Specifically, the online retail sales of physical goods were 2,805.3 billion yuan, up by 11.6 percent, accounting for 23.3 percent of the total retail sales of consumer goods.”

-PRC National Bureau of Statistics

Alibaba stands to gain a double-digit tailwind if it can defend its market share.

It should be noted that from Q1 2022 onwards, year-on-year revenue growth each quarter has never exceeded 6%.

While growth is slower compared to the go-go years a decade earlier, multiple success stories still exist in the Chinese ecommerce market.

Recall that Douyin’s ecommerce GMV hit some 2% of GDP in just over two years starting from zero. Kuaishou also managed to reach 1% (or roughly US $140 billion in GMV) by 2023, after 5 years of on-and-off experimentation, starting in 2018.

Unlike its competitors building hundred-billion businesses from scratch in a couple of years, however, Alibaba was behind the curve and losing share.

Falling property prices are positive for consumption in the longer term, despite depressing consumer confidence and spending in the short term.

This is because property prices were unaffordably high in more developed areas and still growing, suppressing consumption in other categories.

For example, over the two decades from 2000 to 2020, prices per square meter grew over 13% CAGR in Shanghai. In contrast, the S&P 500 grew at only 6.5% CAGR over the same period.

An investor could double the S&P 500’s returns by just investing in Shanghai real estate; with leverage, he could quite easily beat Buffett. Thousands became rich off this boom - one of the greatest transfers of wealth in recent history.

In 2015, consumers were using wild tactics to take advantage of this boom, such as applying for multiple credit cards to finance downpayments, and sidestepping purchase quotas through fake divorces.

By 2017, the average property in Shanghai was around 50 years’ median pretax income.

Worse, it was still growing – between 2017 and 2020, housing prices put in another sprint at 14% CAGR.

By 2020, after tax and extremely spartan expenditures, it would take the average person close to a century to pay for the property in full.

Meanwhile, both New York and London’s property-to-income ratio stood at just above 20 times. Outside China, perhaps only Mumbai would have a property-to-income ratio comparable to Shanghai – yet still it stood some 20% lower, roughly on par with Beijing, Shenzhen, Guangzhou…

Chinese culture and the one-children policy exacerbates this issue. Men are expected to own property before marriage, and the country still has one of the highest homeownership rates in the world, at nearly 90%.

Inevitably, many families fund downpayments with six wallets: both the parents of the bride and groom and the couple themselves would chip in.

High property prices are why consumption is low relative to GDP, but also why lower property prices in the longer term unlock larger TAM for Alibaba.

Property prices are lower in lower-tier cities, and much lower in rural regions, but people living in those areas also have much lower incomes and limited spending power.

This underserved lower mass market, combined with the decreased consumer confidence from falling property prices in more developed regions, is why Chinese ecommerce players have recently pivoted to a discount-retail strategy.

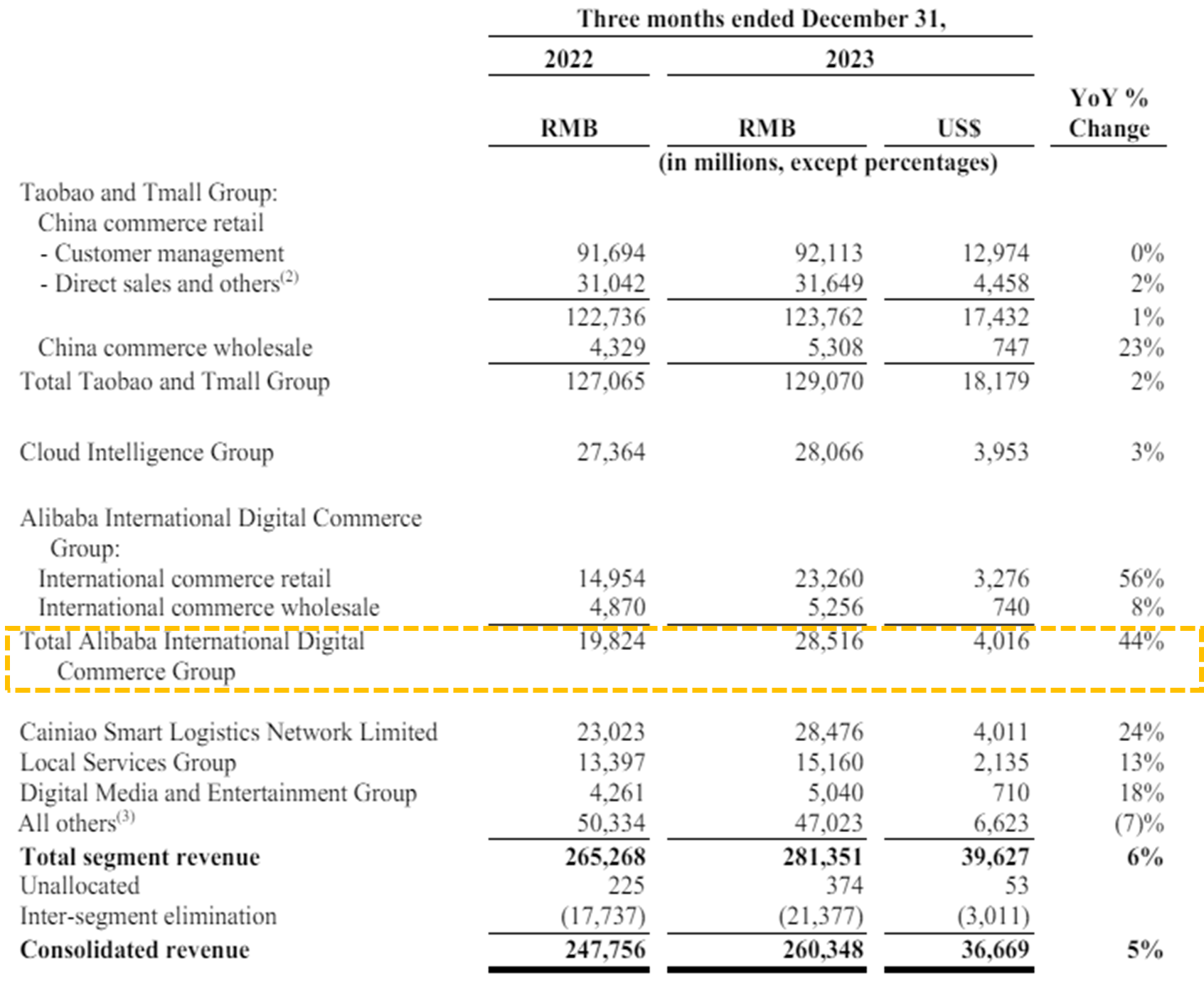

Tariffs and other geopolitical risks. As can be seen from the table below, only around a ninth of Alibaba’s revenues come from outside China.

However, Alibaba’s International Digital Commerce Group did account for some 1/3 of growth. Still, only a subset of this might be vulnerable to heightened import tariff risk, primarily from the US and to a lesser extent the EU

Of Alibaba’s overseas businesses – AliExpress, Alibaba.com, Lazada and Trendyol – AliExpress is likely the most exposed, whereas Daraz and Trendyol are the least but also under $5 billion in revenues combined.

Given the preponderance of its core China business, increased growth there would easily offset lost growth elsewhere.

Delisting risk. This was raised as a risk in July 2022 when the SEC added Alibaba among more than 100 Chinese companies to its delisting watchlist for 2024, but this was mitigated by December that year when the Public Accounting Oversight Board (PCAOB) gained “unprecedented” access to firm audits.

Indeed, BABA ADRs are convertible into HK-listed shares at a ratio of 1:8, which should further protect against this risk.

Of course, any delisting will trigger a sell-off, with some investors only being able to invest in US-listed securities, but some longer-term investors holding HK-listed shares may view this as a buying opportunity rather than seeing this as a lethal no-go.

VIE risk. Variable Interest Entities (VIEs) have long been viewed with suspicion, with some even claiming that they are “illegal” according to PRC law. No Chinese regulator has outlawed VIEs – otherwise those companies would not be still listed as VIEs today.

Rather than expend further time discussing this topic, we would point readers to a pertinent development and encourage independent research: Caixin, a leading Chinese financial news outlet, reported that “China saying complying VIE companies can list overseas”.

Note – this is not legal or investment advice: please consult any legal and investment advisors as required.

Sector Risk

These can be split into:

Sector risk from China

Sector risk from the US and EU

Sector risk from China. In our view, this is already priced in. Many investors struggle to separate several developments that hurt Alibaba’s share price, lumping them all into the black box of “China risk”.

We again show here why business specificities take precedence over macros. Look at the chart below. If you had gone long on JD.com five years ago, you would have been down 1/8, whereas if you were long PDD, you would have been up over 400%.

Ironically, both were net beneficiaries of the “Big Tech crackdown” (vendors were no longer tied to Alibaba, but could now list on JD.com and PDD), yet their share prices diverged as business realities diverged.

Indeed, PDD came under greater pressure than JD, due to its omnichannel grocery business being seen as Big Tech squeezing out the little businesses – more on this later.

The first peak marked the height of the Chinese Big Tech bubble and the crackdown, yet the drawdown from the start of 2024 for PDD marks not China risk, but the US government taking actions against Temu – PDD’s new primary source of growth.

The Big Tech crackdown had three major effects on Alibaba.

First and the most expensive was Ant Financial, costing shareholders some US $67 billion.

From its cancelled IPO in 2020 to the share buybacks in 2023, Ant Financial lost some 70% of its value, declining from $280 billion to $78.5 billion. Alibaba’s 33% stake in Ant Financial means a loss of roughly US $67 billion.

Note here that this was the natural continuation of the regulatory tightening of the fintech sector, especially with regards to consumer loans.

P2P loans were restricted from 2016, but this was from a level of extremely low regulation compared to the US and the EU.

The popular view that Chinese businesses are monolithically state-driven from the top-down is incorrect. In fact, developing sectors tend to be loosely regulated – so when growth trends emerge often dozens or hundreds of entrants would rush into the same space, resulting in a hypercompetitive environment and survival of the fittest.

Ant Financial had built up a business that would not have been permitted in modern day US or the EU, due to this very laissez-faire approach.

It was extending a lot of consumer loans – with over US $300 billion on its books in 2020 – and collecting a lot of the fees yet passing on all the credit risk to banks, building up systemic risk, especially in smaller banks.

Deregulation had already propelled property prices to unsustainable highs – so Jack Ma’s speech acted as the catalyst spurring regulatory action.

Second, the antitrust actions are also over, after a record CN ¥18 billion (US $2.78 billion) fine.

This was for various practices deemed to be monopolistic, such as forcing merchants to sign up to exclusivity clauses and preventing them from selling on other platforms.

The impact of ending such practices is difficult to quantify, though in our opinion would exceed that of the fine itself, since rightly or wrongly, it did form part of Alibaba’s competitive moat.

Incidentally, this was partially catalyzed by an earlier Jack Ma speech extolling the virtues of 9-9-6 (a 72-hour workweek) that drove a public backlash in China, compounded by the likes of PDD and Meituan entering the community groceries space, which used to be the domain of small vendors.

Public sentiment called for the regulation of Big Tech to protect workers against exploitation and small businesses against the giants threatening to squeeze them out. SMEs still form the backbone of the Chinese economy, providing over 60% of total GDP and nearly 80% of jobs.

Third, the silver lining is that Tencent, too, was fined for monopolistic practices and forced to open its ecosystem up to Alibaba.

Again, the impact of this is nontrivial to quantify, though it expands the TAM by both increasing the number of targetable users, but more importantly, the occasions on which users can be reached.

Importantly for investors, the sectors that were hit by crackdowns generally performed extremely well in the years that followed.

Vice stocks – various casino companies and spirits like Moutai declined for one or two years with the crackdown on corruption, yet many doubled or more in the next three to four years.

The private tuition sector provides more recent examples. TAL Education Group was a three-bagger from trough to peak, as was Gaotu Techedu, albeit with a rockier journey. New Oriental was a ten-bagger.

All three put in strong performances in the past year, with the first two gaining 80% and New Oriental gaining over 120%.

Investing in New Oriental in 2022 would have netted savvy investors returns akin to those of Nvidia.

Sector risk from the US and EU. This is more difficult to qualify. While risks like forced divestiture that TikTok might have to contend with are unlikely for Alibaba, there are other trade risks, such as the EU investigating AliExpress when it exceeded the threshold of 45 million MAUs – of a Very Large Online Platform.

Similarly, the US has initiated a Section 301 investigation of China’s maritime, logistics and shipbuilding sectors, which may have implications for Alibaba’s wholesale platform, 1688.com specifically, and sentiments in general.

However, again bear in mind Alibaba’s has limited exposure to international business, which accounts for only a ninth of revenues. Furthermore, international business has yet to reach profitability (segment adjusted EBITA of US -$450 million), still being subsidized by its core China business.

Valuation and Idiosyncratic Risk

We now approach valuation and idiosyncratic risk.

Rather than focusing on ratios like P/B (1.1x for a very asset-light business), or EV/EBITDA (just over 5x), which are broadly known to the market anyway, we like to think of this in terms of three tranches so that we can home in on the growth aspect – which we have established to be the critical determinant of market value for Alibaba:

Value of liquid assets

Value of current business

Value of future business

In Q1 2024 alone Alibaba bought back 2.6% of shares outstanding.

At just under $69, Alibaba’s current market cap works out to be around US $168 billion, yet it had nearly US $92 billion in cash and liquid securities at the end of 2023, which does not include prepayments, receivables or the like.

We are comfortable doing this because Alibaba’s new management has shown it is perfectly happy to do buybacks rather than make further acquisitions.

As a result, the price works out to be roughly US $76 billion for the business itself.

We note that there is just under US $40 billion in intangibles and goodwill stemming from the numerous acquisitions throughout the years. If we extremely conservatively mark this all down to zero in one go, we shall still only be paying $116 million.

Now for the current business. Net income in 2023 worked out to be just over US $10 billion, so we are paying between 7x and 11x earnings (if all intangibles and goodwill are considered to be worthless) if this can be sustained going forward.

Consider, though, valuing the current net income at 8x - this would come out to over $80 billion.

At these rates, we are effectively getting the optionality of growth thrown in for free, with some change to spare.

Recent developments at Alibaba have made us much more optimistic about its prospects, addressing those issues as we highlighted in previous posts.

Recall that we highlighted four key critical challenges for Alibaba – these represented precisely some of the major risks investors were taking on – we are now more optimistic about Alibaba’s prospects, because:

Alibaba’s management has restructured to become more efficient and has made many more big, strategic decisions that would be necessary.

We shall not attempt to enumerate all improvements exhaustively, but provide some information that cannot be easily found elsewhere.

When we spoke to price-sensitive consumers (but who have further spending potential), they are moving back to Taobao & Tmall from PDD.

“I moved to PDD when it became much cheaper than Taobao, but now moved back to Taobao now that I find they’re cheaper at least 3 out of 5 times - and the other 2 times they are either the same price as PDD, or barely more expensive … how do they do it?”

-A high-income Taobao customer

In fact, Alibaba is increasingly shifting from its promo-driven model to an everyday low pricing (EDLP) strategy, de-emphasizing Singles days and spreading promotional periods over more months.

With the above changes, we expect Alibaba to be better able to defend its market share.

Taobao & Tmall also reconciled with Tencent, a key channel for customer acquisition and engagement, levelling the playing field.

The screenshot below demonstrates this perfectly – Taobao is now allowed to advertise even within WeChat.

This is happening elsewhere as well, even offline. Walmart was one of the earliest allies of Tencent, having opened its first store in China, in Tencent’s hometown of Shenzhen. Consequently, Walmart became one of the first chains to boycott Alipay.

Carrefour provides another interesting case. Initially both Alipay and WeChat Pay were accepted. When it allied with Tencent however, Carrefour stopped accepting Alipay 7-8 years ago.

Next, most of its shares were acquired by Suning (in which Alipay was a key shareholder), it shift allegiances to Alipay and stopped accepting WeChat Pay.

Finally, Carrefour became open to both payment methods again - only to shutter almost all of its operations just months later as the business succumbed to the pandemic slump and online competitors.

Renewed focus is clear from the sales of non-core assets – now increased attention is being paid to core business.

This can be seen in the increase in micro-innovations and A/B tests.

Notice how in the screenshot above, Tmall and Taobao added a much larger button to take customers directly to the payments page, and only having a tiny add to cart button in comparison.

Previously, there was only the shopping cart, and no 1-click ordering, which was patented by Amazon until 2017.

This is a much bigger and more strategic change than a first glance would indicate.

Instead of maximizing order size, Tmall and Taobao are now prioritizing stickiness and repurchases, which goes a long way to combat PDD’s previously unique tactic.

Alibaba’s improved competitive actions are already showing promising early signs of conversion into growth.

First, it should of course be noted that revenues declined around 4% from 2022 to 2023, yet Q1 GMV figures give more cause for optimism.

So far so grim. Taobao and Tmall, while having recovered to double-digit GMV growth, still appear to be losing share to competitors right?

Not so fast.

Eagle-eyed readers may have noticed this small yet important line – for Q4 2023, Alibaba’s China ecommerce wholesale segment (its very first core business), was growing nicely.

This was in fact driven by dropshippers from Douyin and Kuaishou. These influencers order goods off 1688.com (the Chinese version of Alibaba.com) – allowing Alibaba to tap into much more impressive ~40% YoY growth from Douyin and Kuaishou.

Such growth is nice, but the wholesale business is still small for the moment (though this still implies US $300-500 million in revenue growth for the whole year if sustained).

More important are the implications. PDD used to be the platform of choice for such dropshippers, yet now they are switching to Taobao and Tmall.

Our main concern would be if major ecommerce players devolve into a prolonged and all-out price war.

The NBS and the postal statistics show that the average value of parcels fell some 26%, which may be partially attributable to deeper discounts, but also the smaller basket size tactic that Taobao is now trying.

We believe that any price wars are unlikely to last for long, because major players are now prioritizing profitable growth over growth alone.

A good example would be the recent price war involving Luckin and Cotti – which lasted for only about half a year.

However, even in a worst-case scenario of an extended price war, Alibaba has the edge – its business model is less cash-intensive, and it has considerably more cash anyway.

Douyin and Kuaishou are not well-placed to directly compete with the other three in terms of pricing. Red has a more premium positioning and limited scale. Meanwhile, JD’s model is too capital-intensive to discount for too long.

That leaves PDD, yet it must devote considerable resources to Temu. Indeed, for March, PDD’s year-on-year growth fell to 13% versus Taobao and Tmall’s 14% - leading to softer March figures for the overall sector in China.

To complete the analysis, if we go back to the first chart, when Alibaba last showed even mid-single digit revenue growth, share prices went to about $100. This would be our rather conservative base case.

In our bull case, if revenue growth can go back to 10-15%, we would expect a two-bagger or even better.

Finally, we see limited downside to Alibaba’s current prices. Going down another 10% from here would see Alibaba hit 1.0x P/B.

Full disclosure: We hold a long position in Alibaba and PDD - this is not a solicitation to buy or sell. We have no current business relationships with the companies mentioned in this note, and are not paid to write this piece (other than paying fellow exponents of the research).

Disclaimer: This should not be construed as investment advice. Please do your own research or consult an independent financial advisor. Alpha Exponent is not a licensed investment advisor; any assertions in these articles are the opinions of the contributors.

Hi, thank you for the analysis! Could you share where you got the data from in the chart “Taobao and Tmall are now again growing GMV at double digits” and also for the later paragraph stating “for March, PDD's year-on-year growth fell to 13% versus Taobao and Tmall's 14%”.

Thank you!